1.06 | How Markets Work

What you are actually buying when you buy a stock, and why the price on your screen is rarely the full story.

Somewhere right now, someone is watching Apple’s stock (or could be any) price tick up and thinking: Good, Apple is doing well today.

Apple does not care. Apple did not receive a single dollar from that trade. The person who sold those shares got the money. Apple went home the same as it started the morning, running factories, writing software, shipping phones to 1.5 billion users who have never once thought about what their purchase does to a ticker symbol.

This is the thing about financial markets that nobody explains to you at the beginning. The stock market and the companies inside it are living almost entirely separate lives. And the moment you understand that separation, everything else about how markets work starts to make sense.

Welcome back to a new episode of Money Flow - How Money Actually Works. Every week, I share one thing I have learned on this journey. Sometimes it is a concept. Sometimes it is a mistake. It is always something I wish someone had told me earlier. And today, finally, we are going to talk about how the market actually works, what it is, what you own inside it, why prices move the way they do, and why almost everyone has the wrong mental model of all three.

If you are new here, the series starts from the very beginning. These are the posts you may have missed:

Start from the beginning

1.01 | Doing Well With Money Is 20% Knowledge and 80% Behavior

1.04 | The Most Expensive Word in Personal Finance Is “Someday.”

Every market starts with a business that needs money

Before there is a market, there is a company.

A company is nothing other than a group of people who decided to make something (goods & services to create value), such as coffee, software, electric cars, streaming content, etc., and charge other people for it.

The logic underneath every single one of them is identical: bring in more than you spend, keep doing that for long enough, and you have built something valuable.

Most of us interact with these companies every day without thinking much about the machinery underneath. When you tap your phone to pay for something, you are moving through the infrastructure of Visa, Apple Pay, and your bank simultaneously, without thinking about any of it. That is fine as a customer.

However, as someone who wants to own a piece of these businesses, though, the machinery is exactly what matters. (We will go deep on how to read that machinery in Series 2.) For now, hold just one idea: a company is a machine that converts effort and capital into profit, year after year.

Now, not every company will let you own a piece of it. Most businesses in the world are private, and that is their right. Their financials are their own business, their decisions are made internally, and no amount of money you offer will get you a share. The only way to invest in them is to know someone on the inside.

SpaceX is the most vivid example of this right now. As of writing this post on May 15, 2026, SpaceX has filed confidential IPO paperwork with the SEC and is expected to open to public investors as soon as June 11, 2026, at a reported valuation somewhere between $1.5 and $1.75 trillion, depending on which estimate you trust. You still cannot buy a share today. The process is underway but not yet complete, and until the day it is, you are on the outside. A company chooses when to open its doors to you. And when it finally does, it happens through a very specific process.

The one moment money actually changes hands between you and the company

On December 12, 1980, Apple opened its doors.

The company worked with two investment banks, sold 4.6 million shares at $22 each, and collected roughly $100 million in fresh capital from the public. That process is called an Initial Public Offering (IPO), an IPO, and it is the only moment in a company’s life when it actually receives money from public investors. Everything that happens after that day is between investors buying from and selling to each other. The company watches from the side.

Here is how it actually works, step by step, because most people have never had it laid out clearly.

Apple works with investment banks to determine a price and structure the offering. Those banks earn fees for this work. This is the primary market, where new shares are being created, proceeds going directly to the company.

The shares begin trading between investors on the open market. This is the secondary market. From this point forward, every transaction is between a buyer and a seller. Apple is no longer involved.

Every time you have bought Apple stock since December 12, 1980, you bought it from another investor who decided to sell. Apple received nothing from that transaction. The price could go up or down a hundred times tomorrow, and Apple’s engineers would still show up to work.

For example, the only money that BMW get is when you buy a car from them for the first time. After that, every time you resell that car to anyone, BMW is not gonna get a penny, and the same thing happens with stocks as well.

This is the distinction almost nobody explains at the beginning, and it changes how you think about price movements completely. A falling stock price does not hurt Apple's operations. It does not reduce their revenue, slow their R&D, or affect the 1.5 billion people using their devices. It only affects the people who own the shares. The company and its stock price are living parallel lives, and understanding that gap is the beginning of thinking like an investor rather than a spectator.

If this is something you are looking to learn, then join me in this journey by subscribing to my mailing list so you’ll never miss any updates & I’ll be motivated to create valuable content for you.

What you actually own, and why companies keep coming back to the market.

So when you buy a share, what did you actually get? A share is a unit of legal ownership in a business. When you own one share of Apple, you own a fractional piece of everything the company earns, holds, and produces. That entitles you to three specific things.

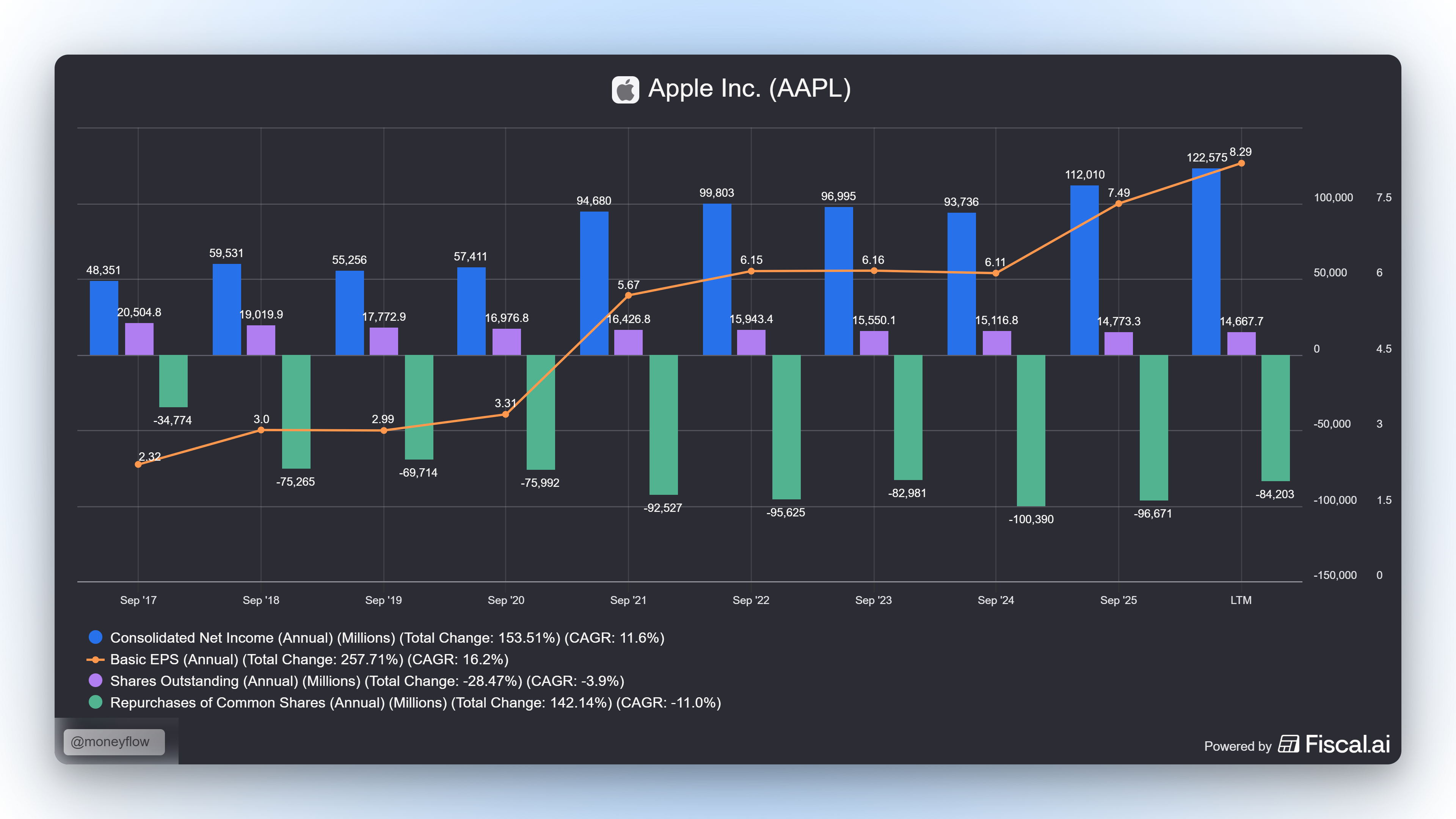

Source: Fiscal.AI

First, a proportional claim on profits. In Apple’s fiscal year 2025, which ended in September 2025, the company earned $112 billion in net income across roughly 14.9 billion shares outstanding. That works out to $7.46 in earnings per share. If you own one share, $7.46 of Apple’s annual profit legally belongs to you. Most of it gets reinvested back into the business rather than paid out as cash, but the claim is real and permanent.

Second, a vote. Shareholders elect the board of directors and weigh in on major decisions. One share is one vote. It is a small voice, but it belongs to you and nobody else.

Third, a residual claim on assets. If the company were ever wound down, shareholders would receive whatever remains after all obligations are settled. This brings up something worth addressing clearly, because it confuses a lot of new investors.

What about bonds and debentures?

A company has two main ways to raise money. It can sell ownership through shares, which is what we have been talking about. Or it can borrow money from the public by issuing debt instruments. When that debt is secured against specific company assets, property, equipment, or receivables, it is typically called a bond.

When it is unsecured, backed only by the company's general creditworthiness rather than specific collateral, it is more accurately called a debenture.

In everyday conversation, particularly in the US and Canada, the two terms get used interchangeably. The important distinction for you is this: bondholders and debenture holders are creditors, not owners. They get paid before shareholders if anything goes wrong. That is exactly why shares carry more risk than corporate debt, and why, over long periods, they have historically delivered higher returns. (I will go much deeper on this in Series 2.)

Now, here is where a question most people have never thought to ask becomes very relevant. If the company does not receive money from secondary market trades, why does it ever issue new shares after the IPO? And why would it ever buy its own shares back?

Sometimes a company needs more capital than its own profits can provide, perhaps to fund a major acquisition, expand into new markets, or pay down debt. In those cases, it can issue new shares to the public and collect fresh capital, the same way it did at the IPO. The cost of doing this is dilution: every existing shareholder now owns a slightly smaller piece of the pie, because more slices have been added. This is why sophisticated investors watch secondary share issuances carefully. It is not always bad news, but it always has a cost that lands on the people who already own the stock.

Buybacks run the mechanism in the opposite direction entirely. When a company has more cash than it knows what to do with, it can purchase its own shares from the open market and retire them. Fewer shares in circulation mean each remaining share represents a slightly larger ownership stake in the same business. If the profits stay the same but the share count shrinks, earnings per share go up automatically. Apple has spent $100,390 Million buying back in 2024 alone. The number of shares outstanding has fallen from over 20,504.8 million in 2017 to 14,667.7 million today. That is the same company generating similar profits, but now distributed across far fewer owners. Each remaining share has become more valuable not because the business dramatically changed but because the denominator quietly shrank.

How does a business become worth more over time, and why does the price lag behind?

This is the question underneath everything else.

Continuing on the same company, if Apple does not receive your money when you buy its shares, and if the price going up does not directly help the business, then what is actually happening when a stock becomes more valuable over time?

Think of it like owning a small apartment you rent out. The building does not change much from year to year. But if the rental income you collect doubles over a decade, the property is worth significantly more to any potential buyer, because it now generates twice as much cash. Investors price businesses the same way. More profit means a more valuable company. More value per share means a higher price.

Add Apple’s buyback strategy on top of that. When profits grow at the same time the share count is shrinking, earnings per share compound faster than either factor alone. That combination is why Apple went from a market value of $1.8 billion on IPO day in 1980 to $4.41 trillion today. The products got better, the profits grew, and the share count was methodically reduced year after year, making each remaining share worth more than the one before it.

That value creation is slow, compounding, and real. It is not driven by the mood of the market on a random Tuesday. It is driven by a business earning more money, year after year, than it did before. Which brings us to the part that trips most investors up.

The gap between price and value, and why it matters more than anything else in this post.

If shares represent real ownership in real businesses, you might expect the price to track the business closely. Over long periods, it absolutely does. But in the short term, prices are driven by something far less rational than business performance.

They are driven by emotion. Expectation. News. Fear. The collective mood of millions of people making decisions simultaneously under uncertainty. And the distance between that mood-driven price and the actual value of the underlying business is where every serious investor looks for opportunity.

When COVID hit in March 2020, the S&P 500 fell 34 percent in 33 days. Apple dropped nearly 30 percent in the same window. Nobody stopped buying iPhones. The services business did not disappear. The engineers showed up to work. What changed was the fear level of the people who owned the shares. Five months later, Apple hit a new all-time high. The business had not dramatically changed. The fear had simply faded.

That gap, between what the market is offering you on a given day and what the business is actually worth over time, is the single most important concept in investing. Price is what you pay. Value is what you get. These two numbers spend most of their lives in different places. Learning to read that gap calmly, especially when everyone around you is either panicking or euphoric, is what separates a real investor from someone who watches prices on a screen.

We will go much deeper on this in Series 2, where we will build out the full Mr. Market framework, talk about how to estimate what a business is actually worth, and look at what Warren Buffett called the most important passage ever written about investing.

For now, carry just this: price and value are different things, and the market confuses them constantly

The scale of what you can actually own a piece of

Now step back and take in the full picture. According to the World Federation of Exchanges, there are over 53,795 companies listed across global stock markets as of May 2025, with a combined market value of approximately $125.71 trillion at the end of February 2024. SIFMA’s Capital Markets Fact Book, using a slightly different methodology, puts that figure at $126.7 trillion for the same year. Either way, the number is genuinely difficult to hold in your mind.

As of January 2025, US stocks alone accounted for approximately $62.2 trillion of that total, meaning the United States, a single country, represents roughly half of all publicly traded value on earth. For context, the next largest markets, China, Japan, and the UK, each account for about 3 to 5 percent. The US crossed the 50 percent threshold of global market share for the first time at the end of 2024.

And here is the thing most people miss when they hear numbers like these. These are not mysterious instruments for sophisticated or brave people. They are the same companies you already buy from every single week. Microsoft. Amazon. Coca-Cola. Netflix. Visa. Unilever. The toothpaste on your bathroom shelf probably belongs to a company whose shares you could own before lunchtime today. Stock markets are not casinos for the financial elite. They are simply the infrastructure that lets everyday businesses invite the public to own a small piece of what they are building.

What to carry forward from this…

By now, you probably know that you do not need a finance degree to participate in markets. You need to understand that you are buying a fractional ownership stake in a real business, run by real people, selling real products to real customers. The price will move every single day. The underlying business moves much more slowly. And over long enough time horizons, it is the business that wins.

In the next post, we will look at the one argument that changed how most ordinary people should think about investing forever, and the specific bet Warren Buffett made to prove it. It is the most practical implication of everything we covered today.

Before any of this becomes actionable, though, there is something more basic that most people skip. All of what we covered today assumes you have money left over each month to actually put to work. Which raises a quieter question: do most people actually know what they take home after all the invisible deductions? That is exactly what Post 1.02 is about, and if you have not read it, that is where the real foundation starts.

If you're liking what I am posting and it resonates with you, then consider supporting me by sharing this post with your family to educate them financially & subscribing to Money Flow. Keep learning | Keep thriving.